A detailed insight was posted to the GARP LinkedIn page (and soon to be added to the P3+ Platform) with the following:

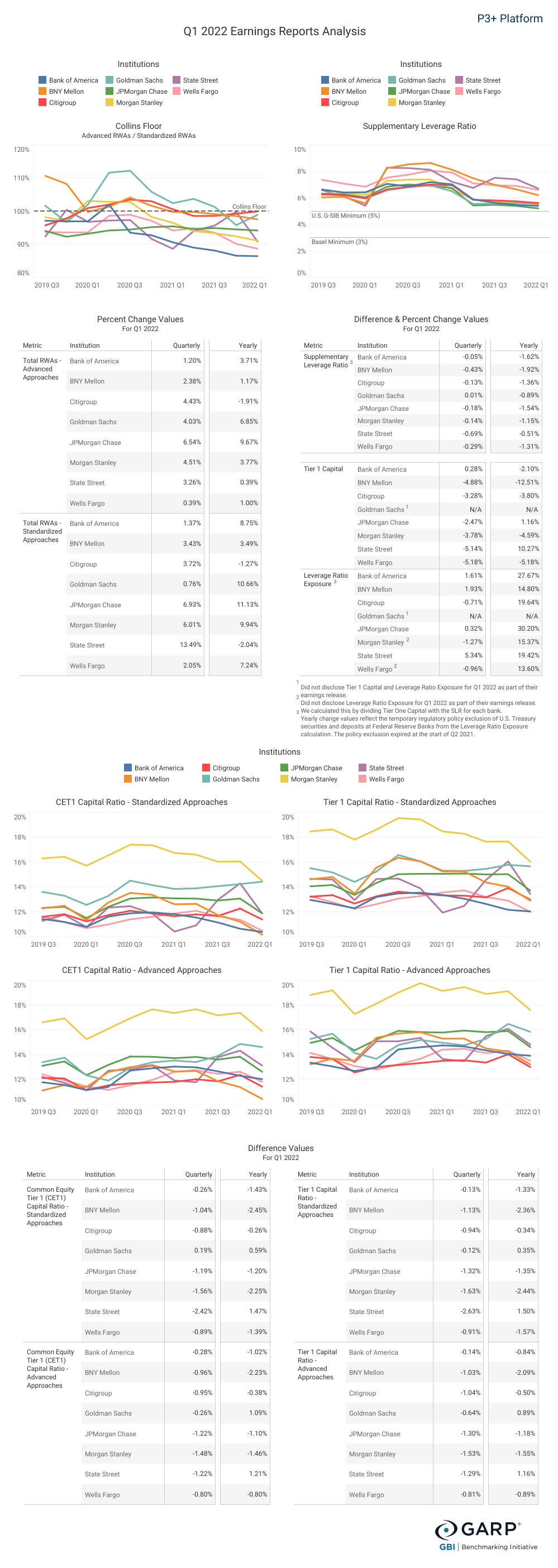

Each of the U.S. G-SIBs posted a further decline in the SLR during the first quarter, with the exception of Goldman Sachs.

The average decline was 24 basis points across all eight banks. JPMorgan saw its SLR move down by 18 basis points to 5.2%, the lowest of the eight and 20 basis points above the 5% policy minimum. The decline was due more to a 2% decrease in JPMorgan’s Tier 1 capital as leverage ratio exposure was essentially flat.

The U.S. Standardized Approach continued to be the binding constraint for each of the U.S. G-SIBs during the first quarter of 2022.

The requirement that each bank use the Standardized Approach for Counterparty Credit Risk (SA-CCR) to calculate exposure amounts for credit risk-weighted assets on derivative contracts effective January 1 proved to be a contributing factor. State Street experienced a noticeable increase in risk-weighted assets under U.S. Standardized during the first quarter partly as a result of adopting the new methodology and which pushed the bank further below the Collins Floor.

A few banks opted for early adoption of SA-CCR, starting with Bank of America in the second quarter of 2020. Goldman Sachs opted for early adoption during the last quarter of 2021 and became bound by U.S. Standardized partly as a result. Morgan Stanley and Wells Fargo both moved further into Collins territory during the first quarter.